Aegis: Bitcoin-Backed Delta-Neutral Stablecoin Without Centralized Counterparty Exposure

Stablecoins have emerged as one of the most crucial pillars of DeFi, forming the backbone of liquidity for trading, payments and yield-bearing products into the crypto realm. With the clearest product-market fit in the space, their utility spans settlement, acting as a pricing asset, and a savings — quietly powering most of the activity behind the DeFi ecosystem.

Broadly speaking, there are two major types of stablecoins: transactional and yield-bearing.

The transactional stablecoins are cash and cash equivalents-backed and generally do not share any yield with their users (examples include Tether’s USDT and Circle’s USDC). The utility of these tokens largely derives from being a settlement currency for volatile pairs (e.g. the vast majority of the perpetual trading volume on Binance is USDT-denominated, while the deepest liquidity on Uniswap for wBTC on Ethereum is against USDC).

The yield-bearing stablecoins compete against each other on a risk-adjusted return basis, where the end user compares the expected yield of each issuer/strategy to technical complexity, longevity and dependencies on counterparties and economic risks. The core primitives in the vertical include tokenized t-bills by issuers like Ondo, Mountain and Usual; spot interest rates derivatives via collateralized debt positions (CDPs) like Sky Money’s sUSDS or K3 Capital’s sBOLD; and tokenized delta-neutral strategies like the cash-and-carry trade by Ethena’s sUSDe. Each of these protocols offer a different level of counterparty and smart contract risks, and perform best during specific market conditions.

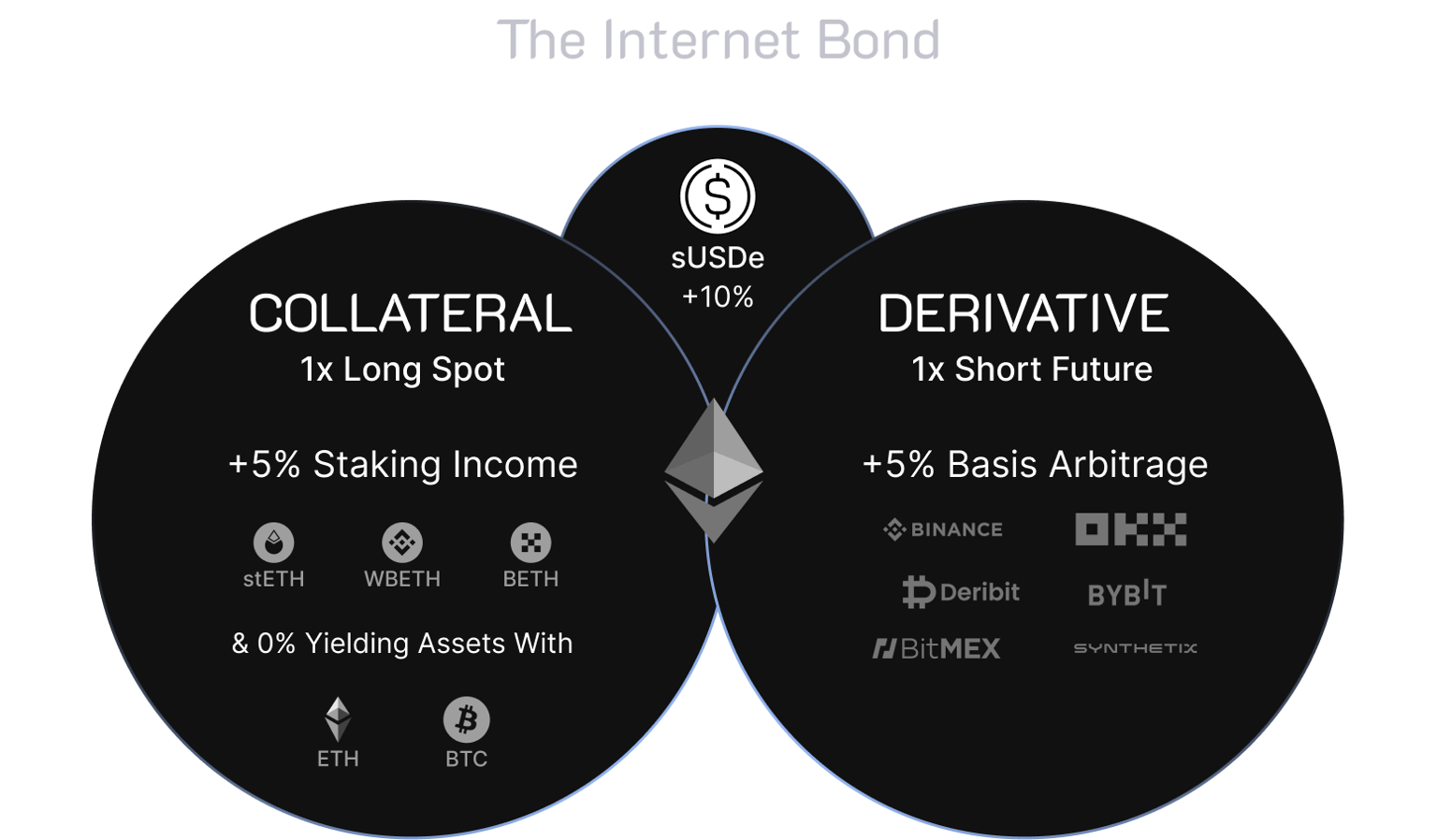

In July 2023, the team at Ethena Labs dropped a billion-dollar stablecoin business idea, aiming to create a crypto-native “Internet Bond” that is censorship-resistant, scalable, and stable. Within just three months of USDe’s public launch in February 2024, its circulating supply crossed the one billion mark, showing a strong product‑market fit and introducing a fresh design paradigm to the stablecoin space.

USDe is a crypto‑native stablecoin backed by a delta‑neutral strategy on top of spot ETH and BTC holdings coupled with an equivalent notional value of short position denominated and collateralized with USDT and USDC. sUSDe is Ethena’s yield-bearing version, which derives its yield from ETH-based Liquid Staking Tokens (like stETH) on the spot leg and the funding interest rate of the perpetual position (which is set at 10.95% on Binance during normal market conditions). As a result, Ethena effectively democratized one of the oldest and most profitable trades in crypto and traditional finance: the cash-and-carry.

However, as most of the perpetual contracts on the centralized and decentralized exchanges are denominated in USDT and USDC, a substantial portion of Ethena’s collateral still resides in them, exposing users to potential depegs due to failures of TradFi counterparties or hostile regulatory developments.

In this article, we will explore Aegis, a BTC-backed cash-and-carry stablecoin protocol that aims to eliminate the dependency to centralized stablecoin issuers. We dive into its protocol design, the size of the targeted market, go-to-market strategy, peg mechanism, team and risks involved.

Enter Aegis

Aegis takes a straightforward, yet powerful approach to eliminate third-party dependencies by excluding the stablecoin-denominated perps from its investment universe, while also forgoing the staking rewards from issuers like Lido and focusing on BTC collateral exclusively — arguably the most trustless and censorship-resistant asset in the space.

Aegis runs a delta-neutral strategy by purchasing spot BTC and opening an offsetting short positions on coin-margined BTC contracts — a structure where both the margin and the payout are BTC-denominated. As a result, Aegis eliminates direct or indirect counterparty risk exposure toward Tether, Circle, or any other stablecoin issuer. The only counterparty exposure lies with the centralized exchanges themselves—and even then, Aegis uses third-party custody agreements to mitigate that risk.

With coin-margined perps, both margin and profits are denominated in BTC rather than USD. That makes the relationship between open interest, price moves, and funding rate PnL non-linear:

Upside: When BTC rallies, collateral value rises while short exposure (in BTC terms) shrinks — freeing up capacity and cushioning volatility. Funding rate earnings compound directly into the BTC stack, boosting collateral without any stablecoin conversion.

Trade-off: If BTC dumps hard, the same convexity applies in reverse; collateral shrinks as short notional value grows, so margin buffers must be topped up quickly. Liquidation math is trickier because thresholds slide with price.

Aegis addresses the downside by maintaining generous BTC buffers and consistently rebalancing its delta-neutral positions, while preserving the upside of a pure-BTC feedback loop without taking on directional exposure.

How big of a market is Aegis chasing?

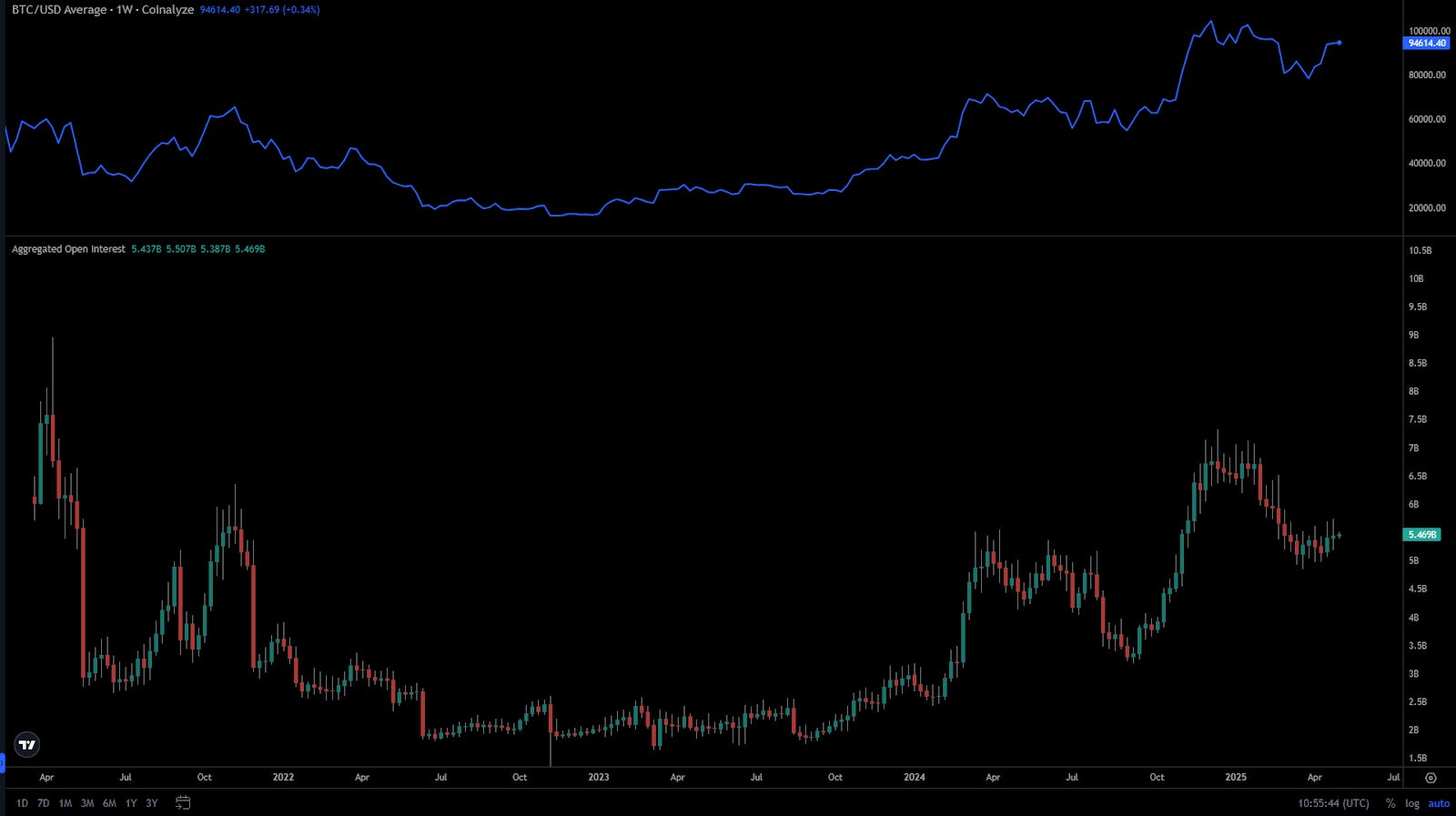

Coin-Margined Open Interest (OI)

Open Interest (OI) represents the total value of outstanding positions in BTC-denominated perpetual contracts. A large and growing OI means more opportunities for Aegis to enter and maintain delta-neutral trades at scale. Higher OI also means Aegis can park larger amounts of BTC in delta-neutral shorts without distorting the funding dynamics.

Note: The aggregated open interest includes only Coin-Margined perpetual contracts on Binance, Deribit, OKX, BitMEX, Huobi, Bybit, and Kraken. USD-Margined perpetuals and all dated futures are excluded.

Based on the data shown above, coin‑M open interest is highly correlated with the BTC price. In bull legs OI ramps quickly as traders add basis exposure. For a delta‑neutral issuer like Aegis this correlation is crucial — large, elastic OI means the protocol can size hedges without crowding markets or distorting funding dynamics. The elastic demand also implies non-linear TVL growth opportunities during market run ups.

As of today’s writing, 5 May 2025, coin‑margined BTC perpetuals carry a combined open‑interest notional of $5.47 billion or ~57,800 in BTC terms.

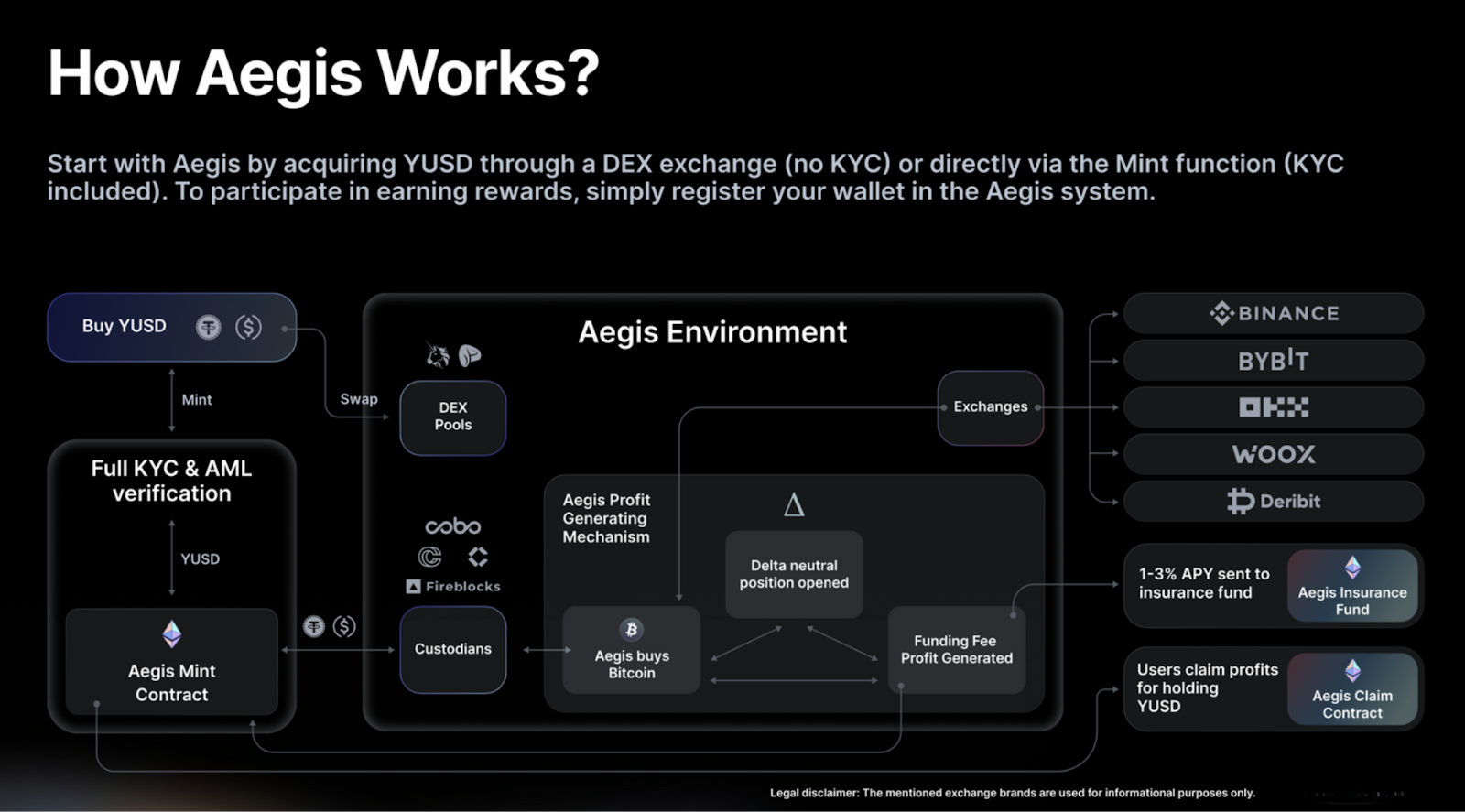

Aegis currently mints YUSD exclusively against stable‑coin collateral — USDT, USDC, or DAI. Every deposit is routed through the Mint Security Layer, swapped into BTC in roughly 15 minutes, vaulted off‑exchange, and matched with an equal‑sized short on a coin‑margined BTC perpetual. Because the long spot‑BTC position and the short perp offset one another, YUSD holders are insulated from Bitcoin’s price swings; their exposure is to funding rate yield, not BTC direction.

This structure also means that a high BTC price (and the typically higher coin‑M open‑interest that comes with it) actually increases the capacity for Aegis to deploy fresh delta‑neutral shorts without crowding the market while creating additional head‑room for future YUSD expansion.

Funding Rates

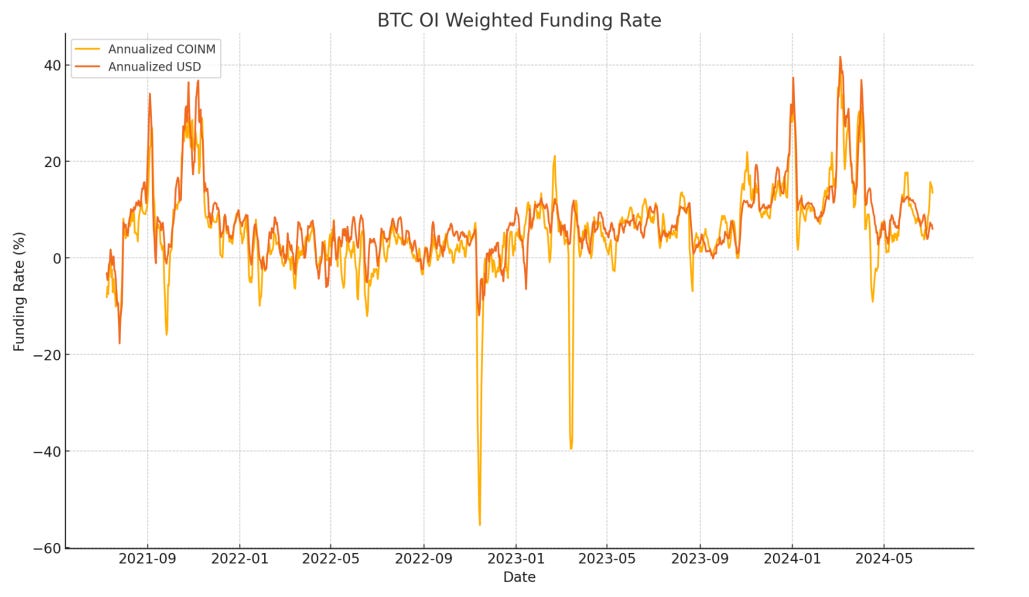

Funding rates are the interest rate exchanged between buyers and sellers of the perpetual derivatives market, aiming to keep its price intact with the spot market. In general, Aegis always sits short on its coin‑margined hedge, the positive funding collected is converted into freshly minted YUSD, which is then allocated to existing tokenholders.

To be sure those flows remain reliable in all market regimes, they conducted an in‑depth stress‑test report on the Insurance Fund, using four years of historical data.

The chart highlights key observations. The BTC-margined funding rate is generally positive across the four years of historical data, spending roughly 78 % of trading days above zero. It is more volatile, but closely correlated to the USD-denominated contracts and in bull phases it can exceed an annualized 40 % APY.

Second, rare but severe drawdowns do occur: episodes such as the 2022 Terra-Luna unwind or the FTX collapse briefly drove annualised funding below negative 50 %. As a precautionary response to those stress windows, Aegis created an Insurance Fund designed to absorb the short‑side carry cost, making sure that the peg will hold steady and ensuring YUSD holders are never forcibly long BTC. The Insurance Fund is allocated by 1 to 5 % of the gross funding income generated by the Protocol based on APY.

Protocol Design

Aegis is designed so a user can progress from merely holding a stablecoin to holding one that automatically earns Bitcoin‑denominated yield — all in a single, seamless flow. In the sections that follow, we’ll break down exactly how Aegis makes that possible.

The primary market requires KYC. Once a user is verified, he/she can mint fresh YUSD directly via Mint contract with a stablecoin of her choice. Stablecoins that are deposited to mint YUSD are sent into an MPC custody with Fireblocks, Copper, or CEFFU — to ensure the highest security and integrity of the assets. After the stablecoins are deposited into the designated vaults, they are available on exchanges through off-exchange settlement to execute spot and short perp trades.

Once the deposit is received, Aegis converts the inflow to BTC within ~15 minutes and mints an equal amount of YUSD to the depositor’s address.

Non-KYCed users can acquire YUSD on the secondary market, tapping the existing DEX liquidity.

Collateral and Risk Management

Aegis’s BTC-only collateral is secured by an institutional-grade custody stack, with funds vaulted in off-exchange MPC custodians, ensuring YUSD’s stability across market regimes.

Off‑Exchange Settlement

Aegis implemented an off-exchange settlement model to ensure user funds are always protected. When Aegis converts mint collateral into BTC, the funds are not held in any exchanges. Instead, assets are vaulted with institutional MPC custodians — Fireblocks, Copper, and CEFFU—who provide battle‑tested key‑sharding, multi‑party approvals, and 24/7 attestations.

Maximum Security: Assets are always held off‑exchange, insulating them from any platform failures or hacks.

Regulatory Compliance: Partner custodians operate under stringent legal and compliance frameworks.

Full Transparency & Control: Users can track every move of their funds in real time—no need to trust an exchange’s balance sheet.

Institution‑Grade Safeguards: Holdings are secured by proven, enterprise‑level MPC vaults and other battle‑tested security measures.

This architecture delivers the depth of centralised venues without inheriting their solvency or security risks.

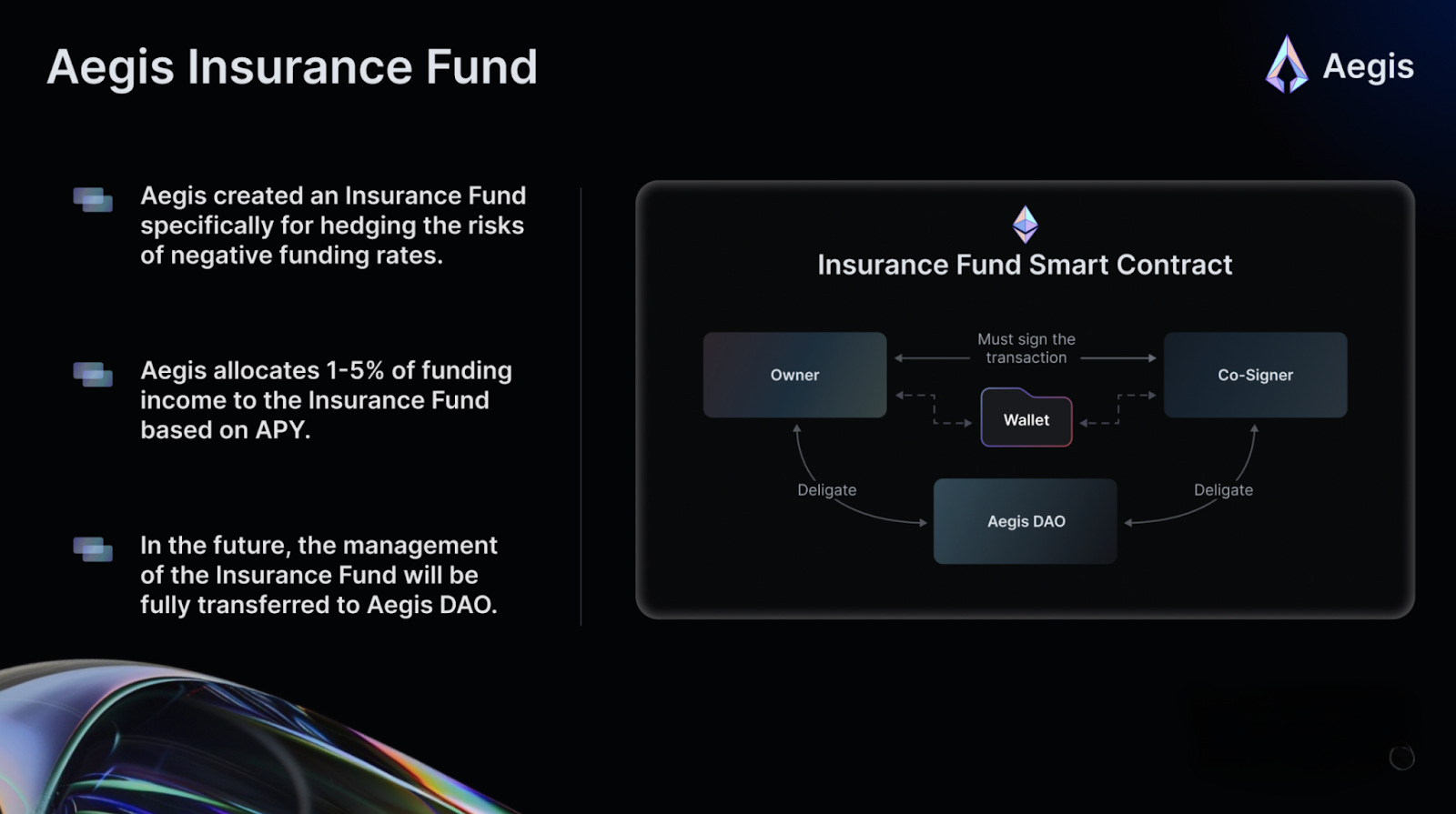

Aegis Insurance Fund

Funding‑rate curves aren’t always positive. To ensure YUSD remains stable when shorts pay longs—or when BTC rips in either direction—Aegis allocates 1–5 % of every funding income into an on‑chain Insurance Fund based on APY.

Dynamic top‑ups. The percentage skim scales with protocol APY: richer markets seed the fund faster, leaner periods preserve holder yield.

Automatic triggers. If cumulative negative funding or hedge rebalancing costs begin to erode collateral ratios, the contract can draw on the Fund to plug the gap long before peg pressure emerges.

Aegis ran simulations using historical funding data from 2020 to 2024—including the March 2020 crash, FTX collapse, and other negative-yield periods. The results indicate that under the current Insurance Fund model (with 30–50% take rates), every stress-tested scenario would have been covered with a buffer of over 5% remaining. Read the full stress test study here

Upon AEG’s governance token launch, the management of the Insurance Fund will be fully transferred to the Aegis DAO, where AEG token holders will be able to vote on fund parameters, allocations, and future upgrades.

Mint Security Layer

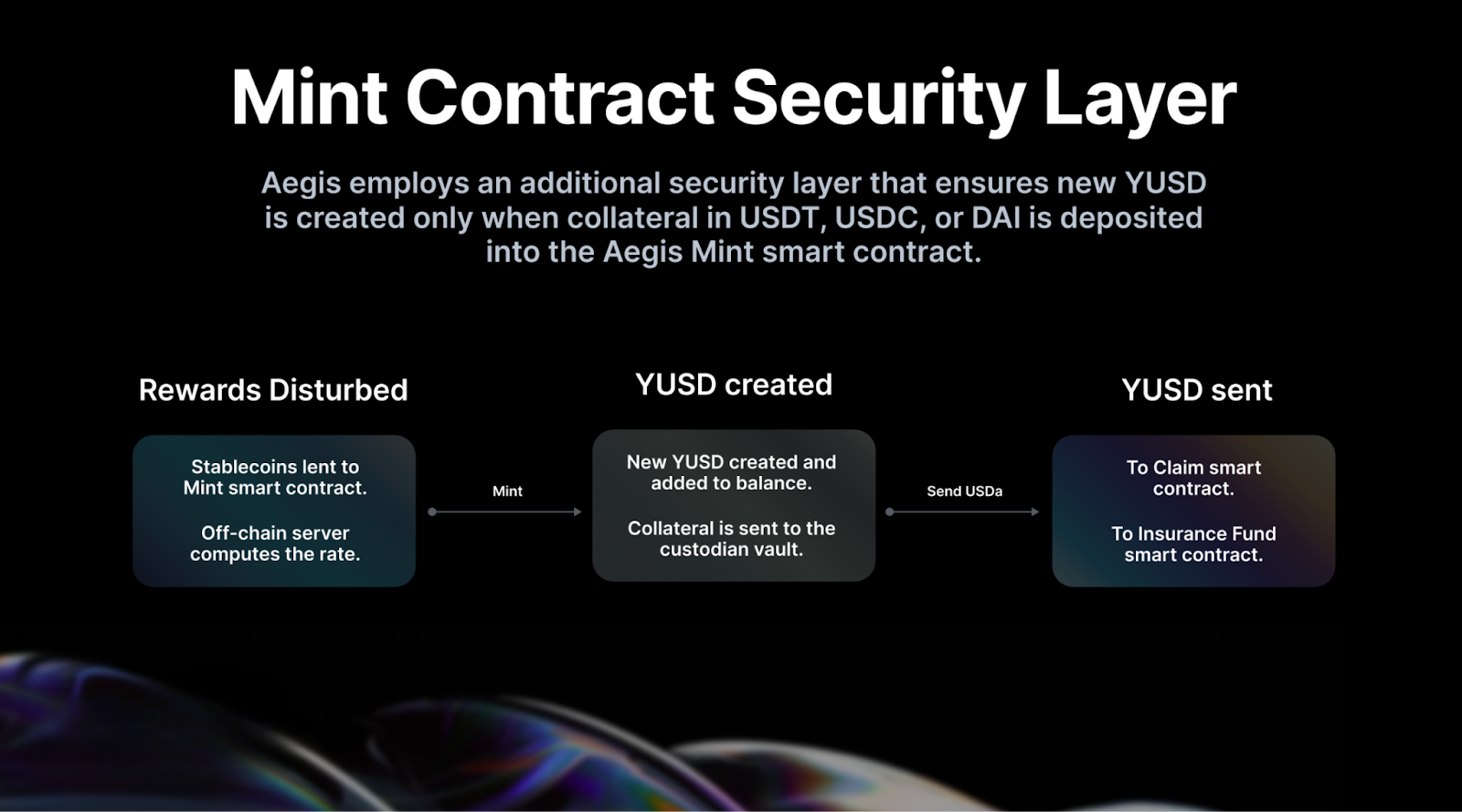

Aegis employs a Mint Contract Security Layer to ensure that every YUSD minted undergoes a rigorous verification process before it can be issued and enter circulation.

Collateral Verification – Before any YUSD is minted, the system verifies that incoming collateral (USDT, USDC, or DAI) is from approved addresses. On-chain analysis tools screen for sanctions or illicit sources. Any suspicious deposits are auto-reverted.

Over-the-Counter (OTC) Conversion – Once verified, the stablecoins are immediately swapped into BTC via trusted OTC desks. This process is optimized for speed (under 15 minutes) and minimal slippage. If the conversion takes too long, the system auto-aborts to reduce risk.

Custodial Security – The freshly acquired BTC is sent directly into a whitelisted vault maintained by a secure custodian. A signed custody receipt is returned and validated on-chain by the Mint contract. No receipt, no mint.

Smart Contract Governance – The entire minting process is enforced by smart contracts that define clear conditions for creating YUSD. This ensures no unauthorized or erroneous mints can occur and all operations remain fully automated.

Transparency & Monitoring – Each step, from deposit to BTC acquisition and collateralization, is fully traceable on-chain. The Aegis public dashboard offers real-time insight, enabling anyone to audit or replay the entire minting history of YUSD.

In short, the Mint Security Layer ensures that every YUSD enters the market over‑collateralized, fully traceable, and shielded from operational or custodial lapses—locking Bitcoin’s resilience into every new dollar created.

Value distribution

Profits generated from funding rate arbitrage and other activities are distributed every eight hours, ensuring regular and timely access to rewards. A slice of those earnings is sent to the Insurance Fund; the rest mints new YUSD that’s distributed to holders.

YUSD holders can claim rewards accrue every eight hours with no staking or lock‑ups. Alternatively, holders can stake YUSD into sYUSD, a yield‑bearing version that auto accrues rewards weekly back into principal; there’s a 7‑day cooldown to unstake back into YUSD.

Aegis maintains YUSD's $1 peg through a deliberately simple and fully transparent arbitrage mechanism. Whitelisted (KYC required) minters could deposit USDT, USDC, or DAI into the Mint contract, mint YUSD at par and sell it on the secondary market when trading at a premium. Alternatively, when YUSD trades at a discount, authorized users can purchase it and redeem YUSD it on a 1-to-1 basis for its underlying collateral, burning tokens and decreasing circulating supply.

Aegis continuously tracks reserve ratios and funding rate health via on‑chain mint/burn data and signed proofs from its custodians and exchanges. If volatility spikes, governance can throttle new mints or tap the Insurance Fund to smooth outliers. Every mint‑and‑redeem hop is logged on‑chain or in audited custody statements, giving anyone the ability to verify collateral balances and peg activity at a glance.

Why this Design Matters

This mechanism is intentionally transparent and incentive-aligned. Controlled supply expands or contracts the moment YUSD strays from $1, and traders earn for keeping the peg tight. Collateral and hedge data are viewable live, so users can see exactly what backs their dollars.

Dual-Token Model

Aegis runs a dual-token model to split utility across two complementary tokens – YUSD and AEG, keeping monetary stability and governance incentives clearly separated.

YUSD — Stablecoin

YUSD is a Bitcoin‑backed, delta‑neutral stablecoin that tracks $1 while passively accruing funding rate income. Because rewards are streamed straight into the token balance every eight hours, simply holding YUSD is enough to earn. No staking contracts, no lock‑ups. For users who prefer automatic compounding can convert to sYUSD; that wrapper rolls each reward epoch back into principal, with a seven‑day cooldown to unstake.

One outstanding feature of YUSD is its real‑time transparency. Every satoshi of reserve BTC, every hedge size, and every Insurance Fund inflow are displayed on a public dashboard. Whether you’re a whale or a casual DeFi user, you can watch collateral movements, funding‑rate PnL, and vault balances tick in real time.

AEG — Aegis’ Governance Token

AEG is meant to serve as the governance token to the protocol. At launch, Token holders will be able to propose and vote on:

Protocol upgrades & new features – technical improvements pushed through community consensus.

System‑parameter adjustments – collateral ratios, venue limits, risk frameworks, and other operational levers.

Treasury & liquidity management – how DAO funds are allocated, liquidity incentives, and Insurance‑Fund top‑ups.

Strategic partnerships & integrations – adding new exchanges, collateral types, or yield strategies.

Asset‑management strategies – deploying Insurance‑Fund assets, adjusting take‑rates, or other yield‑generating initiatives.

Governance is one‑token‑one‑vote. A proposal needs 4 % quorum of total AEG supply and 51 % approval for approval, after which a timelock gives the community a cooling‑off window before execution.

Aegis Points Program (Launched 16 April 2025)

Aegis rolled out a points program aiming to transform the early YUSD holders into protocol owners by offering them a pro-rata distribution of 0.3% (previously 0.2%) of the total future $AEG supply every week, while simultaneously earning stablecoin’s native yield.

The first epoch of the LP and points program will last for 3 months. During this period, users can accumulate points across multiple avenues to maximize future token allocations.

Currently users can earn points via:

Hold YUSD/sYUSD in their wallet

Hold sYUSD YT or provide liquidity on Pendle

Supply YUSD on Euler

Provide liquidity on Curve/Uniswap

Participate in partner money markets

Refer friends (earn 10% of what they earn)

Engage on Discord & X for bonus points

To start earning points today, visit app.aegis.im/earn

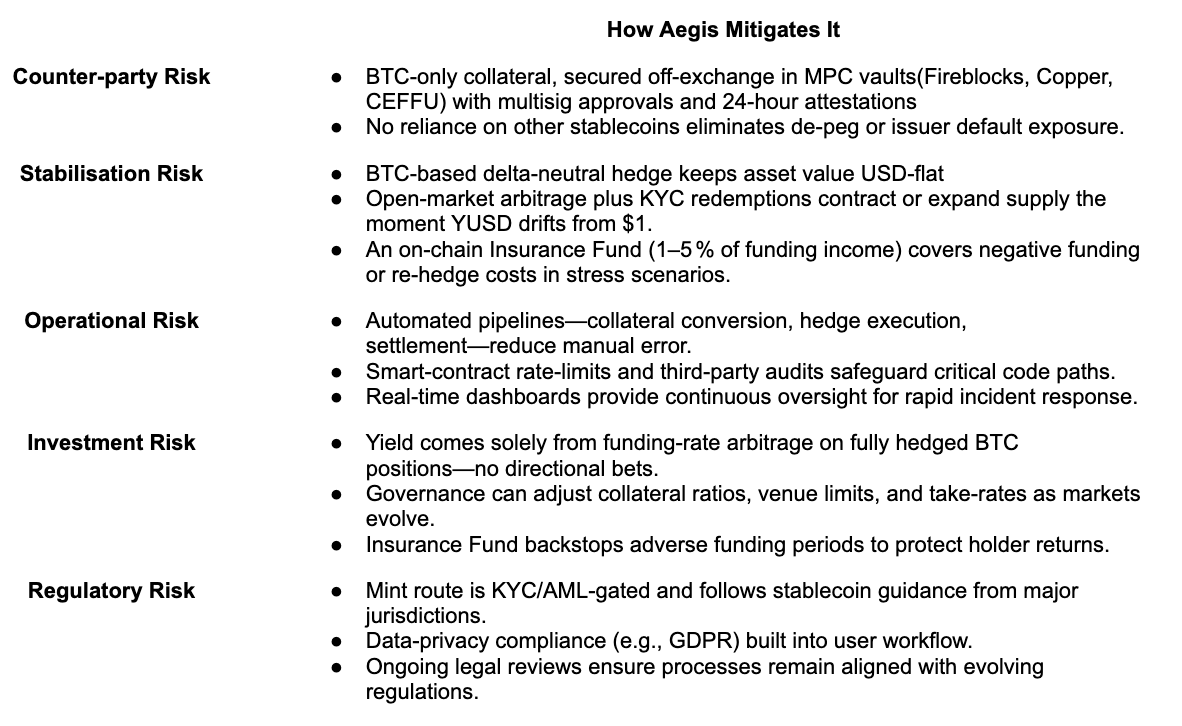

Risks

The Aegis team addresses the risks they might face which would potentially exploit the protocol through 5 different verticals and emphasizes their way to mitigate those risks.

While the core risks above are mitigated by Aegis’s design, one residual consideration remains: the hedge is delta‑neutral in BTC, not necessarily in USD. Because both collateral and PnL are denominated in bitcoin, the dollar value of the book can drift whenever BTC rallies or pulls back. To keep YUSD immunised from this FX noise, the Aegis team must periodically rebalance its short leg—adding or trimming coin‑margined BTC perps whenever spot moves materially or funding‑rate conditions change.

This routine adjustment is baked into the protocol’s operations and is carried out long before peg stability or collateral ratios are threatened, ensuring holders stay exposed to funding‑rate yield, not to bitcoin’s price swings.

Team

Aegis is fully resourced on both the technical and business fronts, led by the following core team members:

Ermin Sharich — Strategy Lead / CBDO and Co-Founder

Co‑founder of Cointelegraph Research, former Auditor & M&A Manager at KPMG, and Senior Institutional BD at Gate.io. Ermin now steers business development and research after investing with Pretiosum Ventures’ $20 million Web3 infra fund.Michael Egorov — Chief Technology and Product Officer

Former CTO at 3Commas DeFi, Michael blends product‑management rigour with deep blockchain know-how, guiding cross‑chain product design and user experience.Alex — Head of Trading & Risk

With 15 years in market‑making and high‑frequency trading (ex‑Riverside), Alex designs the protocol’s hedging and risk‑management framework. He keeps a low public profile for security reasons.Tony — Chief Operating Officer

A serial entrepreneur with 10+ years building tech start‑ups, Tony most recently led a project incubated by Google for Startups. He oversees day‑to‑day operations and go‑to‑market execution.

In addition to the core members, Aegis also receives guidance from three seasoned advisers: Arjun Aurora, COO of Orderly (backed by WOO Network); Jeremy Gruffat, former Business Development Director at Paradigm; and Wilbert Li, who leads the stablecoin ecosystem at Pendle. Their expertise helps steer the project’s strategy and growth.

Conclusion

Aegis solves the core weakness of today’s yield‑bearing stablecoins: reliance on centralized dollar rails. By using Bitcoin for its collateral, margin, and settlement — and hedge with coin‑margined perps, removes exposure to USDT, USDC, and their issuers.

The model is simple but disciplined. Continuous monitoring and swift re‑hedging, backed by MPC custody and a funding‑fed Insurance Fund, keep the peg intact and cover periods of negative carry. Four years of stress‑testing show the fund remains solvent even at a multi‑billion‑dollar YUSD supply.

Crucially, market depth is already sufficient. The market that Aegis is targeting — coin‑margined BTC open interest — sits near US $5.5 billion and historically tracks Bitcoin’s bull cycles. That liquidity lets Aegis scale shorts without crowding venues or compressing funding spreads; each dollar increase in coin‑M OI translates into incremental capacity for new YUSD.

Once the AEG‑governed DAO is live, collateral limits, venue lists, and take‑rates can adjust in real time, keeping risk tight as derivatives liquidity shifts on‑chain.

For allocators who need a stable unit of account but prefer to avoid fiat rails, YUSD now offers a credible alternative: Bitcoin‑collateralized, transparently hedged, and defended by a self‑funding reserve. Provided the team continues to publish real‑time proofs, maintain conservative vault practices, and iterate risk parameters via DAO governance, Aegis is well‑positioned to become the institutional default for “dollar stability without dollar risk.”

X: @k3_capital | @aegis_im For latest update: @k3alpha For contact: @K3Capital